According to a recent report by global consulting firm McKinsey, accelerating electric vehicle demand has increased the need for powertrain electrification components. As such, aftermarket suppliers face both opportunities and challenges as the electrification momentum is growing.

According to the report, EV sales have surged after a standstill during the Covid-19 pandemic. EV sales grew by over 90% between 2020 and 2022 in the U.S. and Europe. In China, this growth was over 300%.

The industry is experiencing a major structural shift as well. McKinsey estimates that about 70% of the suppliers of the automotive third-party, or aftermarket, will consolidate in the next three to five years.

Both original manufacturers and third-party component suppliers are facing several challenges. Those include cost increases in raw materials and electronic parts and a rise in internal costs.

Several shifts have already occurred in the past three years. Among those is a faster acceleration of electrification than was expected. New government policies and investor and consumer demands have increased the pressure on vehicle manufacturers to speed up the transition.

In addition, automotive original equipment manufacturers (OEMs), which are all the major vehicle makers such as Volkswagen, Toyota, Mercedes-Benz, Ford, General Motors, BMW, Honda, SAIC Motor, Hyundai, and Stellantis, are moving more and more toward insourcing of e-powertrain systems and parts.

Meanwhile, demand for the legacy powertrain components for traditional gas and diesel-powered engines is expected to grow through 2025 and then decline.

This might increase costs if e-powertrain components were purchased from third-party or aftermarket manufacturers.

Another trend McKinsey highlighted is that OEMs and aftermarket suppliers increasingly separate internal-combustion engine (ICE) and electric vehicle (EV) businesses. This provides additional cash to finance the transition in the short term.

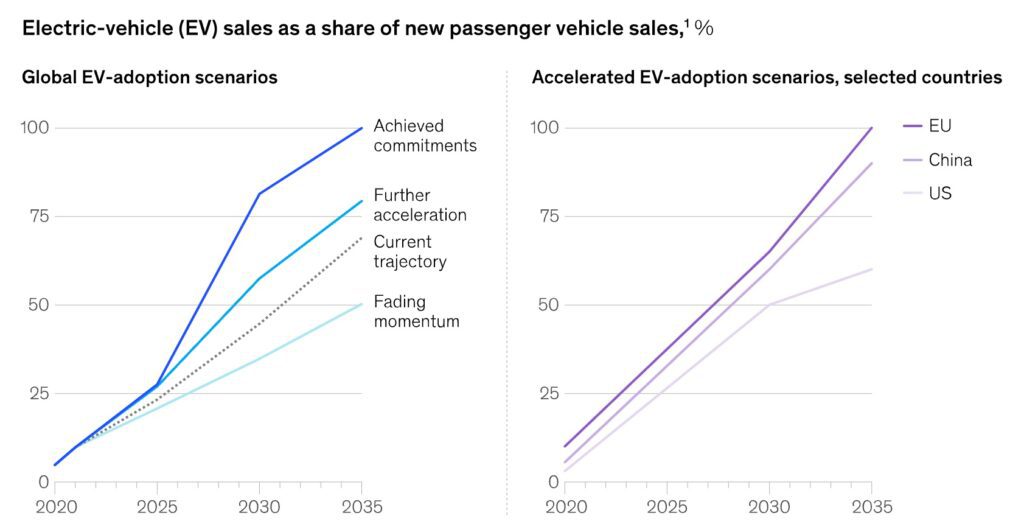

“By 2035, battery electric vehicles (BEVs) will likely represent more than 65 percent of all new light-vehicle sales across the global automotive market,” said the report. “The factors driving sales differ across regions. For example, Europe is experiencing high regulatory pressure, while China feels a strong consumer pull despite reduced incentives. US demand grew to more than 5 percent of new-car sales in 2022, and recent government action is expected to boost the transition to BEVs.”

But the industry is also facing a few challenges. Continued supply chain shortages, a slow buildout of EV charging networks, and the increasing cost of raw materials to make batteries provide short-to-midterm headwinds for the industry.

Because of the accelerating momentum in the EV transition, a joint survey between McKinsey and the European Association of Automotive Suppliers forecasts that there might be increased consolidation among automotive third-party suppliers.

So far, OEMs have announced investments of over $500 billion by 2025 to build in-house electrification systems. The report estimates that the actual expenditure will be much larger.

“…by mid-decade we expect many large traditional OEMs to assemble e-drive units and battery packs in-house and to outsource battery cells and selected power electronic systems, such as DC/DC converters and onboard chargers,” wrote the authors of the report.

This should allow OEMs to further benefit from cost savings and to differentiate themselves from competition. As both OEMs and aftermarket suppliers invest in e-powertrain component manufacturing capabilities, McKinsey expects a major consolidation among the latter.

“A fundamental shift is taking place across the automotive value chain, and it’s happening faster than many in the industry anticipated,” concluded the report. “The impact of the current surge in vehicle electrification has fallen heaviest on the shoulders of the supply base, which faces high levels of uncertainty, shifting customer plans, and the need to secure investment capital.”