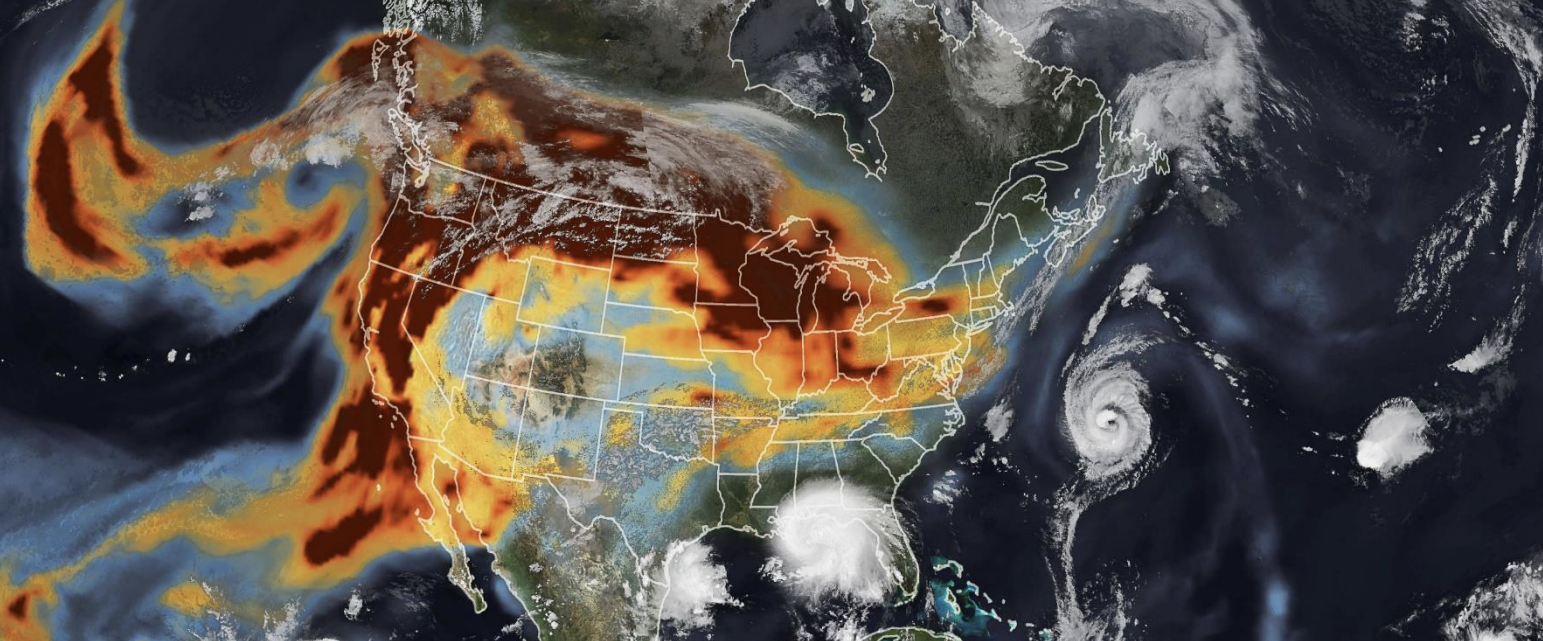

Predicting the weather is an inexact science – except when it comes to how it is impacted by climate change. Climate scientists see a clear connection between global warming and this century’s increase in extreme heat waves, droughts, floods, storm surges, and winter blizzards. It is a near-certainty that extreme weather events will continue to occur well into the future, regardless of whether your local meteorologist whiffs on tomorrow’s forecast.

Extreme weather has become so prevalent that even the business world must account for it in its own risk assessments. As The Wall Street Journal recently reported, this includes designing algorithms that can predict the likelihood of natural disasters hitting specific towns, industrial parks – even individual buildings – and then assessing how much damage they might do.

This kind of information is especially important to holders of municipal, corporate, and mortgage-backed bonds.

According to a white paper published by risQ, a Boston-based firm that models financial risks tied to climate change, current and future climate risk “is an existential threat to the municipal debt ecosystem.”

The white paper notes that most economic climate losses are now absorbed by the public sector, primarily the Federal Emergency Management Agency (FEMA). But FEMA can only shoulder so much of the financial burden before its own coffers are drained. FEMA’s National Flood Insurance Program (NFIP) already owes more than $20 billion to the U.S. Treasury, which leaves only about $10 billion in borrowing authority from a $30.425 billion legal limit.

This means more of the financial risk will fall on municipal bondholders. RisQ is among the firms that aim to analyze and reduce that risk. The company models the complex financial risks posed by climate change and then translates them into actionable insights for municipal debt stakeholders.

RisQ was founded in 2016 as a spinout of Northeastern University’s Sustainability and Data Sciences (SDS) Lab, with funding from the National Science Foundation. Cofounders included Dr. Evan Kodra, who now serves as the company’s CEO; and Colin Sullivan, its chief operating officer.

The company’s model is based on a digital grid that divides the U.S. into 100-meter by 100-meter sections of land and then forecasts the likelihood of climate events in each square. After that, it assigns associated risk scores to the bonds that would be affected.

“Eventually this chicken is going to come home to roost,” Kodra told the WSJ. “It has morphed into a systemic risk that no one person has to worry about when it will hit until it does.”

The importance of risQ’s work caught the attention of Intercontinental Exchange (ICE), the Atlanta-based financial services company that acquired risQ late last year for an undisclosed sum. ICE changed the startup’s name to ICE Data and Innovation Impact Group, though it is still popularly known as risQ.

ICE’s buyout of risQ continued a trend of large financial firms dipping their toes into the climate risk assessment. In 2019, Moody’s acquired a majority stake in California-based Four Twenty Seven, a provider of data, intelligence, and analysis related to climate risks. Meanwhile, Morningstar’s Sustainalytics unit, which provides ESG research and ratings, launched a partnership with rival XDI to assess climate risk in corporate bond markets.

The seeds of risQ were planted in 2014 after Kodra finished his Ph.D. at Northeastern and concluded that a huge gap existed between climate change research and practice. As risQ notes on its website, Kodra found that the insurance sector “generally does not price climate change risks into underwriting.”

He and Dr. Auroop Ganguly, a climate scientist and professor at Northeastern, began exploring the idea of starting a company that would address this gap. A year later, fellow Northeastern alumnus Sullivan, an expert in tech transfer and business development, joined the startup team. RisQ officially launched in 2016 after it received a $225,000 National Science Foundation (NSF) Small Business Innovation Research (NSF SBIR) grant.

Today, risQ lists four fundamental components of its underlying climate risk modeling platform:

- Hazards such as wildfires, floods, and hurricanes, each of which carries a combination of probabilities and intensities that are modulated by climate change scenarios.

- Climate conditioning incorporates projected changes in climate variables that modulate the intensity and/or probability of the above hazards.

- Economic exposure, in which risQ analyzes risk to fundamental economic exposures on its 100-meter grid. For each hazard, risQ quantifies the risk to property value.

Damage functions are designed to translate probabilistic intensities such as flood depth and wind speeds into two areas: expected replacement costs, and expected business interruption as measured by commercial and industrial property downtime.